- Basic

Enquire Us

Sole Proprietorship

A sole Proprietorship is a type of business structure where an individual owns and operates a business as a single entity. In a Sole Proprietorship, there is no legal distinction between the owner and the business, which means that the owner is personally responsible for all aspects of the business, including its debts and liabilities.

Sole Proprietorship is one of the simplest and most common forms of business ownership, particularly for small businesses. It is easy to set up and requires no formal registration with the government. The owner has complete control over the business and can make all decisions on their own.

However, Sole Proprietorship also has some disadvantages, including the unlimited personal liability of the owner. This means that if the business incurs debts or legal issues, the owner’s personal assets, such as their house or car, may be at risk. Additionally, a Sole Proprietorship may have limited access to funding and resources compared to larger business structures, such as partnerships or corporations.

Advantages and disadvantages of Sole Proprietorship

| Advantages of Sole Proprietorship | Disadvantages of Sole Proprietorship |

| 1. Simple and easy to set up | 1. Unlimited personal liability |

| 2. Complete control and autonomy | 2. Limited ability to raise capital |

| 3. Minimal legal and regulatory requirements | 3. Limited lifespan |

| 4. Owner receives all profits | 4. Difficulty in attracting top talent |

| 5. Flexibility in decision-making | 5. Heavy workload and long hours |

| 6. Tax benefits | |

| 7. Privacy |

Filing taxes for a Sole Proprietorship

If you have a proprietorship firm, you are required to file tax returns every year unless you are exempted. In this type of business, you and your firm are considered as one entity. The type of tax return form that needs to be filed depends on the nature of your proprietorship.

If your firm is run by a Hindu Undivided Family (HUF) or any individual proprietor, you need to use Form ITR-3 to file your income tax.

On the other hand, if you want to reduce the compliance burden for your small business, you can file your proprietorship tax using Form ITR-4 under a presumptive tax scheme. This way, your business income is added to your personal income and your business taxes become your personal taxes.

As a proprietor, you are entitled to the same tax deductions as individuals or HUFs.

How to Verify the Registration Status of a Proprietorship in India?

In India, there is no central registry or database to check the proprietorship status of a business. However, you can verify the registration status of a proprietorship firm by checking the following documents:

- PAN Card: Every proprietorship firm is required to have a PAN (Permanent Account Number) card, which is issued by the Income Tax Department. You can check the status of the PAN card by visiting the official website of NSDL or UTIITSL and entering the PAN number.

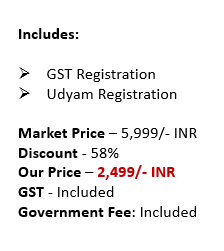

- GST Registration Certificate: If the proprietorship firm is registered under the Goods and Services Tax (GST) regime, you can verify the GST registration status by visiting the official GST portal and entering the GSTIN (GST Identification Number).

- MSME Registration Certificate: If the proprietorship firm is registered under the Micro, Small and Medium Enterprises (MSME) Act, you can check the registration status by visiting the official Udyog Aadhaar portal and entering the Udyog Aadhaar number.

- Trade Licence: The proprietorship firm may also require a trade licence from the local municipal corporation or Panchayat. You can verify the status of the trade license by contacting the relevant authorities.

In addition to these documents, you can also check the proprietorship status by conducting a background check and verifying the business details through reliable sources such as government websites, business directories, and professional associations.

Step-by-Step Guide to Obtaining GST Registration for a Proprietorship in India

If you are a proprietorship in India and want to register for GST, the process is straightforward and can be completed online through the GST portal. The first step is to visit the GST portal (www.gst.gov.in) and click on the “New Registration” option. You will need to provide your PAN, mobile number, and email address, and then enter the OTP to proceed. After that, you will need to fill out the necessary details, such as business type, owner details, and bank account details.

Once you have entered all the necessary information, you will need to upload the required documents, including PAN card, Aadhar card, and bank statement. Finally, verify the details and submit the application. After submitting the application, you will receive an Application Reference Number (ARN) for your application.

Your application will be processed, and if everything is in order, your GST registration certificate will be issued within 3-7 working days. Once you have your GST registration certificate, you will be able to legally collect GST from your customers and avail of GST input tax credits. It is essential to note that GST returns must be filed on a regular basis, and failure to comply can result in penalties and legal action.

Mandatory Compliance: Income Tax Return Filing for Proprietorship Firms?

Yes, it is necessary for proprietorship firms to file income tax returns in India. Under the Income Tax Act, every person who earns income in India is required to file income tax returns if their income exceeds the specified threshold limit.

In the case of proprietorship firms, the income earned by the business is treated as the income of the proprietor, and therefore the proprietorship firm is required to file income tax returns. The proprietorship firm can file income tax returns using Form ITR-3 or Form ITR-4, depending on the nature of the business.

Filing income tax returns is not only a legal requirement but also an important financial discipline. By filing income tax returns, the proprietorship firm can claim various deductions and exemptions allowed under the Income Tax Act, which can help in reducing tax liability. Filing income tax returns also helps in building a good credit score and provides proof of income for various financial transactions such as loans, investments, and visa applications.

Therefore, it is advisable for proprietorship firms to file income tax returns regularly and ensure compliance with tax laws and regulations.

Opening a Bank Account for a Proprietorship Business in India: A Step-by-Step Guide

To open a bank current account for a proprietorship in India, the account will be opened in the name of the business owner using their PAN. The business owner must submit proof of doing business by providing any two of the following documents:

- GST registration certificate

- Shop & Establishment Act licence

- A licence issued by the Registering authority such as a Certificate of Practice issued by the Institute of Chartered Accountants of India, Institute of Cost Accountants of India, Institute of Company Secretaries of India, Indian Medical Council, Food and Drug Control Authorities, etc.

- Importer Exporter Code (IEC) issued to the proprietorship concerned by the office of DGFT can also be accepted as an identity document for opening a bank account.

These documents are required to create a current account instead of a savings account in the name of the proprietorship. Banks may have additional requirements or procedures for opening a current account for a proprietorship, and it is advisable to check with the specific bank before proceeding with the account opening process.

Legal and Regulatory Compliances for Proprietorship Firms

Proprietorship firms in India are required to comply with various legal and regulatory requirements. Here are some of the key compliances that a proprietorship firm needs to adhere to:

- GST Returns: If your proprietorship firm is registered under the GST regime, you need to file monthly or quarterly GST returns depending on the turnover.

- Income Tax Returns: Every proprietorship firm is required to file income tax returns annually. The due date for filing income tax returns is usually 31st July for the previous financial year.

- TDS Returns: If your proprietorship firm is deducting tax at source (TDS) from payments made to vendors or contractors, you need to file TDS returns on a quarterly basis. The due date for filing TDS returns is the 31st of the following month.

- Professional Tax Returns: If your proprietorship firm has employees, you need to deduct and deposit professional tax to the respective state government and file professional tax returns periodically.

- Other Compliances: Depending on the nature of your business, you may also need to comply with other regulations such as environmental laws, labour laws, and industry-specific regulations.

It is important to ensure timely compliance with all the applicable regulations to avoid penalties, fines, and legal disputes. You can consult a professional or seek legal advice to ensure compliance with all the relevant laws and regulations.

Comparison Table Of Proprietorship, Partnership Firm, Llp And Private Limited Company

Each type of business entity has its own advantages and disadvantages, and the choice between them depends on the specific needs and goals of the business owner. Proprietorship is ideal for small business owners who want to have complete control over their business, while Partnership Firms are suitable for businesses with two or more owners who want to share profits and losses.

LLPs are ideal for businesses that require limited liability protection and a separate legal entity, while Private Limited Companies are suitable for larger businesses that require more members, capital, and compliance.

| Feature | Proprietorship | Partnership Firm | Limited Liability Partnership (LLP) | Private Limited Company |

| Number of Members | Only one owner | Minimum 2 partners | Minimum 2 partners | Minimum 2 shareholders, Maximum 200 |

| Legal Entity Status | Not a separate entity | Not a separate entity | Separate legal entity | Separate legal entity |

| Liability Protection | No limited liability | No limited liability | Limited liability protection | Limited liability protection |

| Registration | Not required | Not required | Required | Required |

| Minimum Capital Requirement | No minimum requirement | No minimum requirement | No minimum requirement | INR 1 Lakh or as prescribed |

| Taxation | Taxed at personal rate | Taxed at personal rate | Taxed at a flat rate of 25% | Taxed at a flat rate of 25% |

| Annual Compliance | Minimal compliance | Minimal compliance | Moderate compliance | More compliance requirements |

| Transfer of Ownership | Not allowed | Allowed with restrictions | Allowed | Allowed |

Related Guides

ITR Services

Other Services

Documents Required

The documents required for the registration of a proprietorship firm in India are as follows:

- PAN card of the proprietor: A copy of the proprietor’s PAN card is required to register a proprietorship firm.

- Identity proof: Any valid government-issued identity proof such as an Aadhaar card, voter ID, driving license, or passport can be submitted.

- Address proof: Any valid government-issued address proof such as an Aadhaar card, voter ID, driving license, passport, or utility bills (electricity bill, telephone bill, etc.) can be submitted.

- Bank account proof: A canceled cheque or bank statement in the name of the proprietor is required.

- Business registration certificate: Depending on the type of business activity, a registration certificate may be required from the relevant regulatory authority. For example, for food-related businesses, an FSSAI registration certificate may be required.

- Rental agreement or property ownership proof: A rental agreement or property ownership proof is required if the business is being operated from rented or owned premises.

- Digital Signature Certificate (DSC): A DSC is required to sign the application for registration of the proprietorship firm.